Introduction

The bedding market is expanding into a larger, more segmented sleep economy, with clear leaders by region, channel, and product type.

What stands out most in the latest bedding market statistics is that growth is steady, but the biggest gains are coming from specific subcategories and digital channels.

Use this data-rich breakdown to see how fast the market is moving, which segments dominate, and which brands and financial benchmarks signal where the industry is headed next.

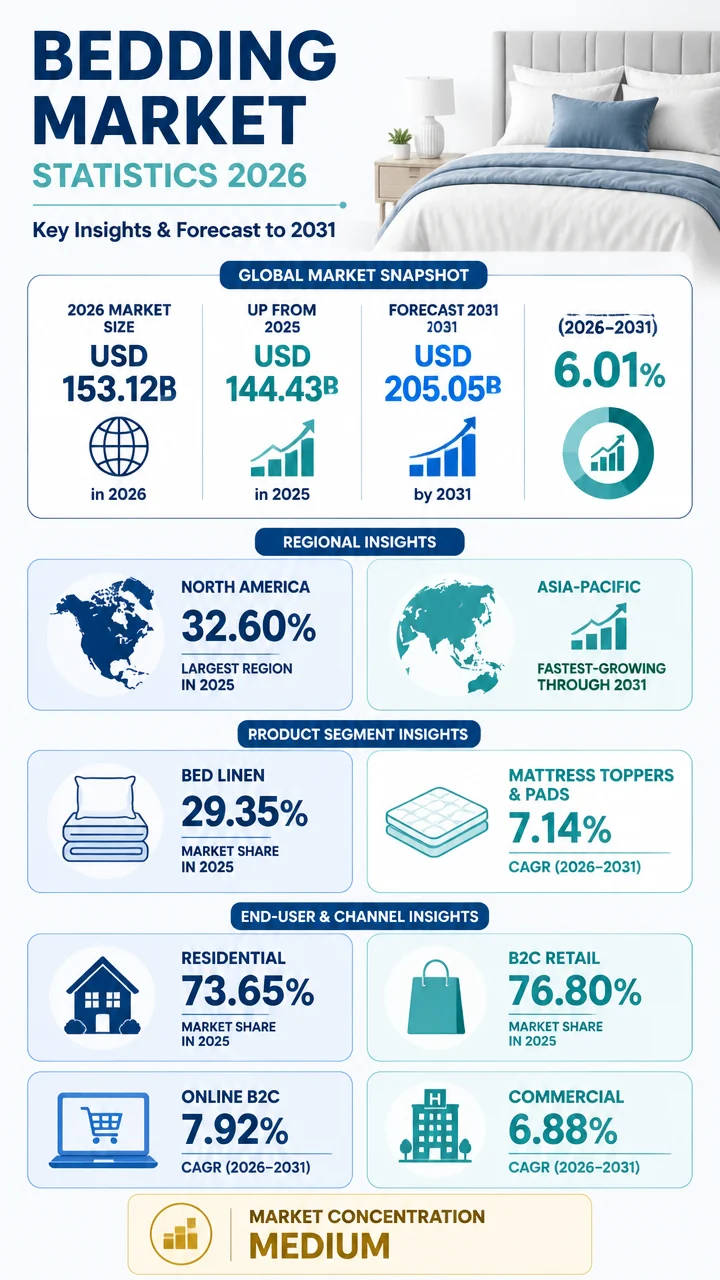

- The global bedding market is projected to rise from USD 144.43 billion in 2025 to USD 153.12 billion in 2026.

- By 2031, the market is expected to reach USD 205.05 billion.

- North America leads the market in 2025, while Asia-Pacific is the fastest-growing region through 2031.

- Residential users and B2C retail dominate today’s demand mix.

- Online B2C is growing faster than the broader bedding market, signaling a continued channel shift.

At a glance: bedding market statistics in 2026

| Metric | Latest figure | What it suggests |

|---|---|---|

| Global bedding market size | USD 153.12 billion in 2026 | The category continues to scale steadily year over year |

| 2031 market forecast | USD 205.05 billion | Room for long-run expansion remains substantial |

| 2026-2031 CAGR | 6.01% | Growth remains healthy, not explosive |

| Largest region | North America | The market is still anchored by mature demand |

| Fastest-growing region | Asia-Pacific | Future growth is shifting toward emerging and scaling markets |

| Largest product segment | Bed linen at 29.35% share | Core textile categories still dominate demand |

| Largest end-user group | Residential at 73.65% share | Home demand is the backbone of the market |

| Largest channel | B2C retail at 76.80% share | Consumer-facing sales still control the category |

| Fastest-growing channel | Online B2C at 7.92% CAGR | Digital purchasing behavior keeps gaining ground |

USD 61.93 billion is the market’s implied growth from 2026 to 2031, based on the move from USD 153.12 billion to USD 205.05 billion.

Bedding market growth statistics and forecast trends

The global bedding market is forecast to grow from USD 144.43 billion in 2025 to USD 153.12 billion in 2026. That one-year increase shows an industry that is still expanding even as consumers become more selective about product quality, comfort, and channel preference.

Mordor Intelligence projects the market will reach USD 205.05 billion by 2031, with a 6.01% CAGR from 2026 to 2031.

That combination points to durable mid-single-digit growth rather than a short-lived spike.

Bedding is a recurring purchase category with replacement cycles, household demand, and commercial use cases.

The CAGR suggests the market is benefiting from all three, not just one growth engine.

- 2025 market size: USD 144.43 billion

- 2026 market size: USD 153.12 billion

- 2031 forecast: USD 205.05 billion

- 2026-2031 CAGR: 6.01%

IMARC’s broader home bedding market view adds another layer of context.

It values the market at USD 103.41 billion in 2024 and forecasts USD 167.59 billion by 2033, with a 5.51% CAGR from 2025 to 2033.

Across reports, the message is consistent: bedding is a large, steadily compounding market with no sign of saturation.

| Research source | Market size / forecast | CAGR | Coverage angle |

|---|---|---|---|

| Mordor Intelligence | USD 144.43 billion in 2025 to USD 205.05 billion by 2031 | 6.01% | Global bedding market |

| IMARC | USD 103.41 billion in 2024 to USD 167.59 billion by 2033 | 5.51% | Global home bedding market |

| Grand View Research | USD 33.42 billion in 2024 to USD 50.56 billion by 2030 | 6.9% | Global bedroom linen market |

Pull quote: “The bedding market is growing across every major lens—global value, channel shift, and premium product mix—but the fastest gains are still coming from the digital and Asia-Pacific sides of the business.”

Bedding market regional statistics: North America vs Asia-Pacific

Regional leadership is one of the clearest takeaways in the bedding market statistics.

North America is the largest bedding market in 2025, holding 32.60% of the global share, but Asia-Pacific is the fastest-growing region through 2031.

That pairing matters because it shows a classic market transition: mature markets still drive current revenue, while developing and rapidly scaling regions shape future growth.

- North America share: 32.60% in 2025

- North America status: Largest market in 2025

- Asia-Pacific status: Fastest-growing market through 2031

- Asia-Pacific CAGR: 7.05% through 2031

| Region | 2025 position | Share / growth figure | Interpretation |

|---|---|---|---|

| North America | Largest market | 32.60% share | Current demand leadership |

| Asia-Pacific | Fastest-growing market | 7.05% CAGR | Future expansion engine |

IMARC also notes that Asia Pacific currently dominates the home bedding market in its framework, reflecting how different report scopes can highlight different leadership dynamics.

In practical terms, both sources point to the same strategic theme: Asia-Pacific remains central to growth, while North America continues to be a major revenue base.

- IMARC’s Asia Pacific coverage includes China, Japan, India, South Korea, Australia, Indonesia, and others.

- Its North America coverage includes the United States and Canada.

Bedding market product mix statistics: which categories lead?

Bed linen held 29.35% of the bedding market share in 2025, making it the single largest product segment in Mordor Intelligence’s view.

That’s a strong signal that foundational textile purchases still anchor the market more than accessories or add-ons.

The category mix also shows where growth may accelerate next.

Mattress toppers and pads are projected to expand at a 7.14% CAGR through 2031, slightly ahead of the overall market and a sign that comfort-enhancement products may gain momentum faster than basic replacements.

- Largest product segment: Bed linen at 29.35%

- Fastest-growing product segment: Mattress toppers and pads at 7.14% CAGR

- Large-volume subcategory: Sheets and mattress covers at around 43% of the bedroom linen market in 2024

| Product segment | Stat | What it says about demand |

|---|---|---|

| Bed linen | 29.35% share in 2025 | Core replacement demand remains central |

| Mattress toppers and pads | 7.14% CAGR through 2031 | Comfort upgrades are outpacing the market |

| Sheets and mattress covers | 43% of bedroom linen market in 2024 | Functional essentials dominate the textile mix |

Grand View Research reinforces the importance of basic linens: sheets and mattress covers accounted for around 43% of the bedroom linen market in 2024.

That concentration suggests shoppers still prioritize everyday essentials over decorative or niche items.

Bedding market end-user statistics: residential demand dominates

Residential end users held 73.65% of the bedding market share in 2025. That is an overwhelming majority and the clearest sign that the category remains primarily household-driven.

Commercial demand is smaller today, but it still matters.

Commercial end users are projected to grow at a 6.88% CAGR through 2031, which is faster than many mature consumer categories and suggests hotels, rentals, and institutional buyers continue to support steady replenishment demand.

Residential demand gives the bedding market stability, while commercial demand adds a second growth layer through hospitality and other bulk-purchase channels.

| End-user segment | Share or CAGR | Strategic takeaway |

|---|---|---|

| Residential | 73.65% share in 2025 | The market is home-first |

| Commercial | 6.88% CAGR through 2031 | Institutional demand is still expanding |

- Residential demand creates the largest base for repeat purchases.

- Commercial demand supports bulk ordering and recurring replacement cycles.

- Product durability and maintenance needs become more important in commercial settings.

Grand View’s bedroom linen data also points to the importance of commercial demand: commercial applications accounted for around 52% of the bedroom linen market in 2024.

Together, the reports suggest that commercial usage is especially important in certain linen subsegments even if residential purchasing dominates the broader bedding market.

Bedding market channel statistics: B2C retail still rules, but online is accelerating

B2C retail channels commanded 76.80% of the bedding market share in 2025. That makes bedding a strongly consumer-led category, with most sales still flowing through retail experiences, either physical or digitally facilitated.

Still, the shift toward online buying is one of the most important bedding market statistics to watch.

Online B2C is projected to grow at a 7.92% CAGR through 2031, outpacing the overall market and suggesting the channel mix will keep tilting toward e-commerce.

76.80% is the share controlled by B2C retail in 2025, highlighting how dominant consumer-facing sales remain.

| Channel | 2025 share / growth | What it means |

|---|---|---|

| B2C retail | 76.80% share in 2025 | Retail remains the primary go-to-market engine |

| Online B2C | 7.92% CAGR through 2031 | Digital discovery and purchase are accelerating |

Grand View Research’s bedroom linen report provides useful context here as well: offline sales accounted for around 67% of the bedroom linen market in 2024.

Even as online gains momentum, physical retail still accounts for the majority of category sales in many bedding and linen submarkets.

- Offline remains large because shoppers often want tactile product evaluation.

- Online growth benefits from assortment depth, price comparison, and direct-to-consumer convenience.

- Retailers that blend physical and digital channels appear best positioned to capture both current share and future growth.

Bedroom linen market statistics and benchmark shares

The bedroom linen segment helps explain how the broader bedding market behaves in practice.

Grand View Research estimates the global bedroom linen market at USD 33.42 billion in 2024, with a projected rise to USD 50.56 billion by 2030 and a 6.9% CAGR from 2025 to 2030.

That forecast sits near the higher end of the major bedding market growth estimates, showing that subsegments tied to everyday use and replacement cycles can still outperform the wider market.

| Bedroom linen benchmark | Statistic |

|---|---|

| Market size in 2024 | USD 33.42 billion |

| Forecast by 2030 | USD 50.56 billion |

| CAGR, 2025-2030 | 6.9% |

| Largest region in 2022 | Asia Pacific |

| Sheets and mattress covers share in 2024 | around 43% |

| Commercial applications share in 2024 | around 52% |

| Offline sales share in 2024 | around 67% |

Bedroom linen is one of the clearest proof points that bedding demand is both essential and replacement-driven, not just trend-driven.

Bedding market concentration and competitive structure

Mordor Intelligence classifies bedding market concentration as medium.

That’s an important competitive signal because it implies the market has recognizable leaders without being fully dominated by one or two players.

A medium-concentration market often rewards brands that can combine distribution, brand trust, and category specialization.

The company data in this dataset supports that reading.

- Large players operate at national or global scale.

- Category specialists can still grow through product focus and channel expansion.

- Retail breadth and margin discipline matter as much as top-line growth.

Bedding industry company statistics: what public filings reveal

Public company filings show how bedding economics play out at the brand level.

Three companies in the dataset—Somnigroup, Purple, and Culp—illustrate different parts of the value chain, from retail and mattress distribution to direct-to-consumer sales and fabric supply.

Somnigroup: scale, margin expansion, and global stores

Somnigroup reported 2024 net sales of USD 4,930.9 million, nearly flat versus USD 4,925.4 million in 2023.

More importantly, profitability improved: gross profit increased to USD 2,180.1 million from USD 2,128.7 million, and gross margin rose to 44.2% from 43.2%.

- 2024 net sales: USD 4,930.9 million

- 2024 gross profit: USD 2,180.1 million

- 2024 gross margin: 44.2%

- 2024 operating income: USD 634.2 million

- 2024 adjusted operating income: USD 721.3 million

| Somnigroup metric | 2024 | 2023 |

|---|---|---|

| Net sales | USD 4,930.9 million | USD 4,925.4 million |

| Gross profit | USD 2,180.1 million | USD 2,128.7 million |

| Gross margin | 44.2% | 43.2% |

| Operating income | USD 634.2 million | USD 607.2 million |

| Adjusted operating income | USD 721.3 million | USD 695.1 million |

Somnigroup also ran over 2,800 retail stores globally in 2024, including over 2,200 Mattress Firm and retail stores in the U.S. and over 200 Dreams locations in the U.K. The company expected the divestiture of 73 Mattress Firm retail locations, 103 Sleep Outfitters specialty mattress retail locations, and seven distribution centers in 2025.

That store footprint underlines how important physical retail remains in bedding, even as online channels grow.

| Somnigroup geography | 2024 net sales | Gross margin |

|---|---|---|

| North America | USD 3,788.9 million | 40.4% |

| International | USD 1,142.0 million | 56.9% |

Somnigroup’s international gross margin of 56.9% was notably higher than its North America gross margin of 40.4%, showing how mix and geography can materially shape profitability in bedding.

Purple: e-commerce still matters, but wholesale is larger

Purple’s 2025 net revenues were USD 468.7 million, down from USD 487.9 million in 2024.

Even so, the company improved gross profitability, with gross profit percentage rising to 40.2% from 37.1%.

Purple’s results show that revenue softness can coexist with margin improvement when pricing, channel mix, or cost control improves.

| Purple metric | 2025 | 2024 |

|---|---|---|

| Net revenues | USD 468.7 million | USD 487.9 million |

| Gross profit percentage | 40.2% | 37.1% |

| Marketing and sales expense | USD 147.0 million | USD 171.3 million |

| Advertising spend as a share of net revenues | 12.0% | 13.4% |

Purple’s 2025 revenue mix was spread across USD 182.842 million in e-commerce revenue, USD 207.387 million in wholesale revenue, and USD 78.496 million in showrooms revenue.

In 2024, the company said DTC sales were 58.1% of net revenues and wholesale sales were 41.9%.

- The company also expanded Mattress Firm coverage from about 5,000 mattress slots to a minimum of 12,000 slots in 2025.

- Purple said its products were represented in Mattress Firm’s full store network in 2025.

- Its sleep products category includes mattresses, pillows, bases, foundations, sheets, mattress protectors, blankets, and duvets.

Purple is a useful reminder that bedding competition is no longer just about product design.

It is also about distribution access and channel economics.

Culp: softer demand and restructuring pressure

Culp’s consolidated net sales fell 13.5% in the third quarter of fiscal 2025 versus the prior-year period, showing how quickly bedding-adjacent manufacturing can feel demand swings.

- Consolidated net sales: down 13.5% year over year in Q3 fiscal 2025

- Mattress fabrics sales: down 4.6% in Q3 fiscal 2025

- Mattress fabrics sales: down 4.2% in the first nine months of fiscal 2025

- Inventory: USD 48.6 million as of January 26, 2025

- Inventory turns: 3.8 in Q3 fiscal 2025

| Culp metric | Figure | Notes |

|---|---|---|

| Accounts receivable | USD 23.1 million | Compared with USD 21.1 million as of April 28, 2024 |

| Days’ sales outstanding | 39 days | Up from 36 days in the fourth quarter of fiscal 2024 |

| Accounts payable – trade | USD 32.7 million | As of January 26, 2025 |

| Capital expenditures, first nine months of FY2025 | USD 2.4 million | Down from USD 3.2 million in FY2024 |

| Restructuring expense | USD 6.3 million | Includes plant and operational consolidation costs |

Of Culp’s USD 6.3 million restructuring expense, USD 2.7 million related to consolidating mattress fabrics operations from Quebec to North Carolina.

The rest included USD 1.5 million of impairment and accelerated depreciation, USD 1.4 million of employee termination benefits, and USD 849,000 of lease termination costs, partially offset by a USD 174,000 gain on sale and disposal of equipment.

Bedding market statistics by theme: what the numbers say together

When the full dataset is grouped together, several clear patterns emerge.

- The market is large and still growing: the global bedding market moves from USD 144.43 billion in 2025 to USD 153.12 billion in 2026 and toward USD 205.05 billion by 2031.

- Home demand dominates: residential users hold 73.65% of the market.

- Retail still leads distribution: B2C retail commands 76.80% share.

- Digital is the fastest channel: online B2C grows at 7.92% CAGR.

- Regional momentum is shifting: North America leads now, but Asia-Pacific grows fastest.

- Core bedding still wins: bed linen is the largest segment at 29.35% share, while sheets and mattress covers account for around 43% in the bedroom linen market.

- Commercial usage adds a second layer of demand: it remains smaller than residential in the broader market but is meaningful in linen applications.

The bedding market looks mature on the surface, but the data says otherwise: growth is real, channel mix is changing, and premium comfort products are still finding room to expand.

Bedding market statistics FAQ-style insights for readers and buyers

What is the current size of the bedding market? Mordor Intelligence forecasts USD 153.12 billion in 2026.

How fast is the bedding market growing? Mordor projects a 6.01% CAGR for 2026-2031, while IMARC and Grand View show similarly strong growth in narrower or differently defined bedding segments.

Which region leads the bedding market? North America is the largest bedding market in 2025, with 32.60% share.

Which region is growing fastest? Asia-Pacific is expected to be the fastest-growing region through 2031, with a 7.05% CAGR.

Which product category leads? Bed linen leads with 29.35% share.

Which channel is growing fastest? Online B2C is projected to grow at 7.92% CAGR.

Which end-user segment dominates? Residential, with 73.65% share.

What’s the most important commercial takeaway? Bedding remains a market where essentials dominate, but growth is increasingly concentrated in upgrading, convenience, and omnichannel buying behavior.

Pull quote: “Bedding is still a household essentials market at its core, but the fastest growth is coming from comfort upgrades, online channels, and Asia-Pacific demand.”